The Unit Economics of Information

Where business information really sits, and what happens to it now.

I have spent the last 20 years selling business information to executives at multinational companies. Not data, not news, but a structured kind of insight that companies pay for to underwrite decision making. Most of it was focused in China, on China, and the insight was delivered through reports, presentations and CEO roundtables.

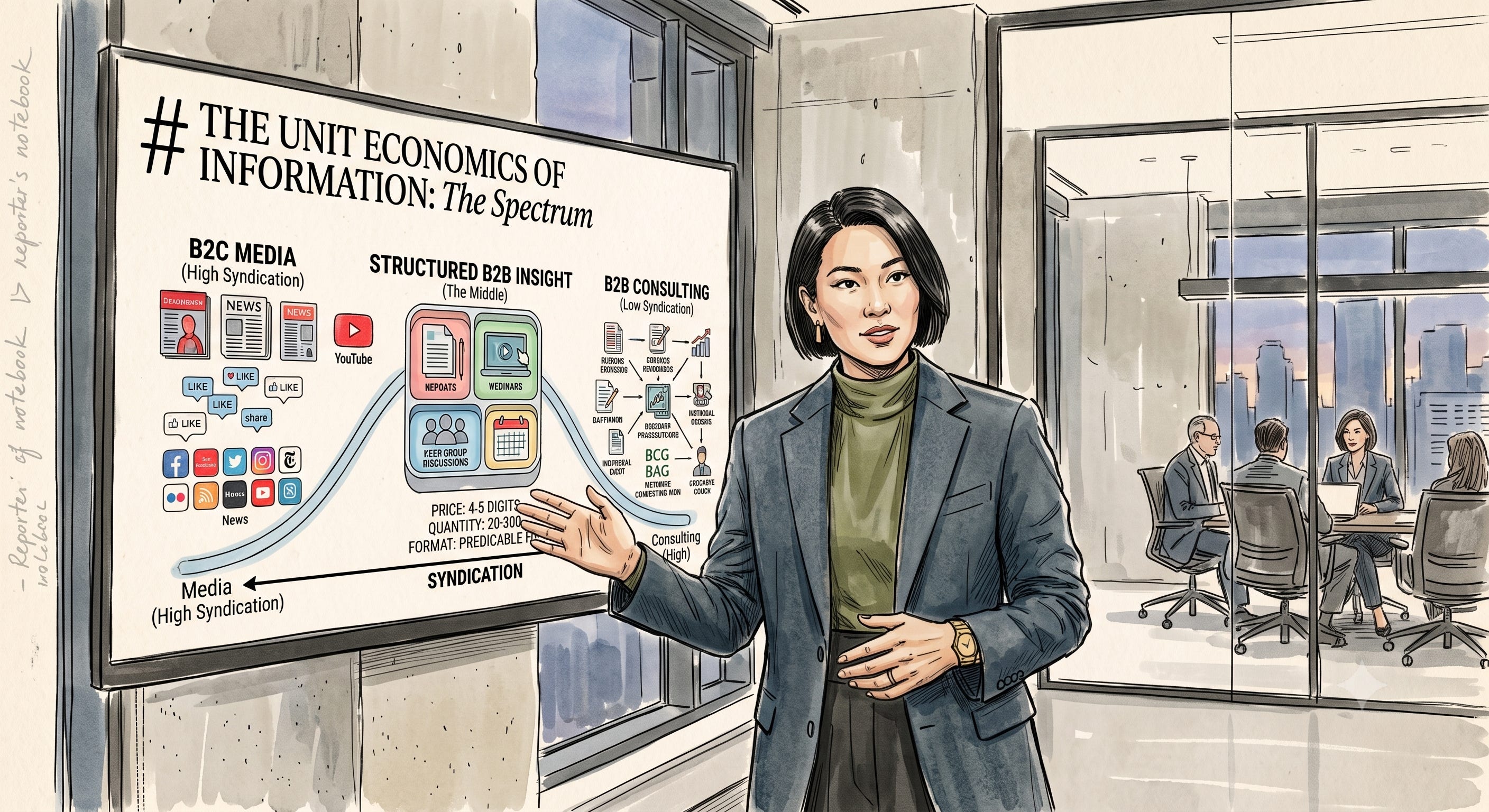

Early on I developed a private framework for it which I call the unit economics of information. The unit economics of information is a framework that maps every insight business onto a single spectrum, from mass-formatted B2C media at one end to fully bespoke B2B consulting at the other, with a product’s position determined by how many buyers share the same deliverable. It was my way of explaining where business information services actually sit, because they sit in between the two.

The spectrum

At one end sits B2C information. At the other extreme sits B2B consulting. The axes are reversed between them. On the B2C side the price is somewhere between 0 and 2 digits, but the quantity can be 5, 6, 7, 8, even 9 digits. Beyond that you are into hyperscaler territory. Flip to the other side. Take the local office of a global management consulting network, or a boutique firm, and it runs the other way around. They might have 10 or 20 clients, maybe 100, but the projects go from 5 to 7 digits.

Photo by Felicia Buitenwerf on Unsplash

On the B2C side, format is everything. Facebook is blue. The Economist is red. The eight o’clock news starts at eight o’clock and does not start five minutes late. On the consulting side, where the work is high-end and bespoke, it is almost format-agnostic. You can present in PowerPoint or Prezi and nobody cares; what matters is that the project is delivered to spec. There are no contracts on the B2C side either. You click on the app store, you buy the paper at the kiosk, you tune in to the World Cup. When the product is free it is paid for by advertising, but we all know that and it is beside the point. With consulting, the contract specifies the deliverables.

In the middle sits the space where I have spent my career: structured B2B insight. Memberships, subscriptions, peer group programmes. The format is predictable, which is what makes the economics work, but the experience is designed to feel bespoke. I have always thought of it as the bento box. You know the compartments, you trust the quality, and you can go a la carte later if you want more.

What determines a product’s position on this spectrum is syndication: how many buyers share the same deliverable. One buyer, and you are fully bespoke, at the consulting end. A million, and you are fully formatted, at the media end. 40 buyers of roughly the same thing, and you are somewhere in the middle. The more people who receive the same insight, the more the format leads and the price falls. The moment specificity becomes essential, format gives way to bespoke, project-based work.

If I have lost you, here is an example. Say you want ideas about how to move your career forward. You are 35. You can pick up your favourite outlet and read a columnist who writes about careers, or follow someone on Instagram who does the same. They deliver in a fixed format, one to many. It might help a little, but not much, because they do not know you or what you need. The next level up is the space in the middle: you join a programme, a set number of sessions, with one coach or with twenty other people in the room, for a one-off fee, a subscription or a membership. And all the way at the bespoke end is a personal coach whose entire job is you.

to bespoke B2B consulting.")

Where peer groups sit

Now take the product I know best, the one I have built and sold for years: the facilitated executive peer group, whether P&L owners or a function-specific cohort, meeting on a regular basis under the Chatham House rule, working through problems with people who genuinely understand them.

Here the price is 4 or 5 digits. The quantity usually runs between 20 and 200, depending on whether it is a tight peer group or a larger forum. The service comes with predictable parameters: you get X meetings a year, Y calls with the team, Z reports.

Behind every session sits a good deal of effort. Understanding each member’s situation, preparing the materials, pre-interviewing participants, designing the agenda, moderating the room, writing the summary, chasing the follow-ups, introducing the members who ought to know each other. A good peer group director carries a whole collection of relationships in their head and works them constantly.

The beauty of the model is that it borrows the format-led structure of B2C content and blends it with the bespoke instincts of B2B consulting. It tries to take the best of both worlds. And if it does neither well, it falls by the wayside and becomes a nice-to-have. That line, between making a real difference and not, is a fine one.

The format is what lets the member know what they are getting into. You get your X, Y and Z. You sign a form, usually one page. You are invoiced up front and you commit to a year. If you do not like it you do not renew, but the expectation on both sides is a multi-year relationship. On top of that you trust that the service will actually help you solve problems. Not fully bespoke, because that is a different price altogether, but close enough to the feeling you get as the client of a consulting firm. That is the balancing act the provider has to pull off: an efficient, streamlined operation that delivers real value at a sensible cost, while still giving every member an experience that feels like theirs alone. There are many ways to systemise that, and many ways to get it wrong.

What’s next in a world with accelerating AI?

Everything I have just described rests on one quiet assumption: that the work wrapped around the insight is scarce, and therefore worth paying for. That assumption is now moving, and with it, the unit economics of information across the whole spectrum. This is the question I want to explore in Augmented Ideas, across strategic intelligence, the executive exchanges where insight gets traded, and the innovation ecosystems forming to act on it.

The signals are already visible in the market for information itself. Gartner’s shares fell more than 20% in a single day in early February 2026, hitting a 52-week low, after the company guided for barely 2% revenue growth in 2026 and management described a tougher selling environment, with clients deferring decisions in a landscape being reshaped in part by AI (TIKR). The stock now trades roughly 70% below its all-time high. Days later, Forrester announced it is exiting its strategy consulting business altogether and cutting around 8% of its workforce, after a year in which revenue fell 8% and contract value, its core subscription metric, declined 6% (The Globe and Mail).

That is not a peripheral story, and here is the uncomfortable part: these are not businesses at the cheap, formatted end of my spectrum. They are the two best-known syndicated research houses in the world, selling 4- and 5-digit subscriptions to thousands of buyers. They sit squarely in the middle. The squeeze is not starting at the B2C end and working its way up the value chain. It is starting in the bento box.

I remember my economics textbooks in the nineties, where perfect market information was a theoretical ideal: everyone with access to full knowledge, making rational decisions. We do not live there. Our markets are imperfect, even as information keeps getting more digital, more democratised, cheaper and more commoditised, and yet the zone is also getting flooded. In some ways this is a live case study in the unbundling that media analysts like Ben Thompson have chronicled for years: cheap distribution keeps peeling layers off what used to be paid, structured insight. So here is the question I keep coming back to. When the information itself is close to free, and everyone can reach it, what actually differentiates you? What is the insight that lets you act with an unfair advantage over your competitors?